Ferrari: Strategy in Motion

A real-world example of strategic anchors, and an important clarification about inputs vs. outputs

I just finished the Acquired episode on Ferrari, and I was blown away. Acquired is one of my favorite podcasts and I could not recommend it enough. This episode in particular hit me because of how perfectly Ferrari’s turnaround maps to the strategic anchor framework I wrote about over a year ago in WTF is Strategy?. I want to share that example here, but I also want to use the opportunity to clarify something the original post under-emphasized.

Strategy is About Inputs, Not Outputs

When I work with founders on strategy, the single most common mistake I see is confusing outputs for strategy. A founder tells me their strategy is to “grow revenue 3x” or “expand margins to 25%” or “hit $10M ARR by year end.” Those are not strategies. Those are outputs. They describe what the founder wants to be true at some future point which is helpful for sure, but not instructive.

Strategy is the set of inputs you commit to in pursuit of those outputs.

A strategic anchor is an input commitment. Not “we will win,” but “this is how we will win.” Not “we will be profitable,” but “these are the three things we will go all-in on, while we 80/20 the rest.” Once you internalize this distinction, a lot of bad strategy becomes obvious. Most of what gets called strategy in board decks is just a list of desired outputs with no theory of what inputs will produce them.

Which brings us to Ferrari.

Ferrari Before Luca: A Company Unmoored

After Enzo Ferrari died in 1988, Fiat ran the company on autopilot for several years. They applied the Fiat playbook to Ferrari: increase production, share parts with the parent company, cut costs, chase volume. Annual production climbed from around 2,200 cars in 1982 to roughly 4,500 by 1991.

The problem was not that any of those decisions were individually wrong. The problem was that Ferrari had no strategic anchors, so every decision was made in a local, uncontextualized way. Share parts with Fiat? Sure, it lowers costs. But it undermines the technology and craftsmanship that make a Ferrari a Ferrari. Increase production? Sure, it grows revenue. But it dilutes the scarcity that makes a Ferrari special. Underinvest in the F1 team? Sure, it saves money. But it lets the myth starve.

Going back to the vector analogy from the original post, each of these decisions had real magnitude. Each one moved some KPI in the right direction. Cutting costs improved margins for a time. Sharing parts saved on suppliers. Increasing production grew revenue. But none of them was aimed at anything specifically Ferrari. They were the generic levers any large auto company has available, and without anchors to point them at something distinctive, they all defaulted to the same direction: making Ferrari more like every other car company. The cumulative effect was slow-motion brand destruction.

When Luca di Montezemolo returned as Chairman in 1991, the first thing he did was buy a 348, Ferrari’s flagship at the time, just to see how bad things had gotten. His verdict:

“The Ferrari 348 was a shit car. It was the worst car we ever made. Everything was missing. It had no personality. It had no technology. It wasn’t state of the art in anything. It had no power. I was getting beaten off the line by Volkswagen Golfs in a Ferrari.”

He then had Ferrari’s test drivers run a Pepsi Challenge against a Honda NSX. The Honda blew them away. By 1991, demand had evaporated. Ferraris were sitting unsold. The factory had to be furloughed for the first time in company history.

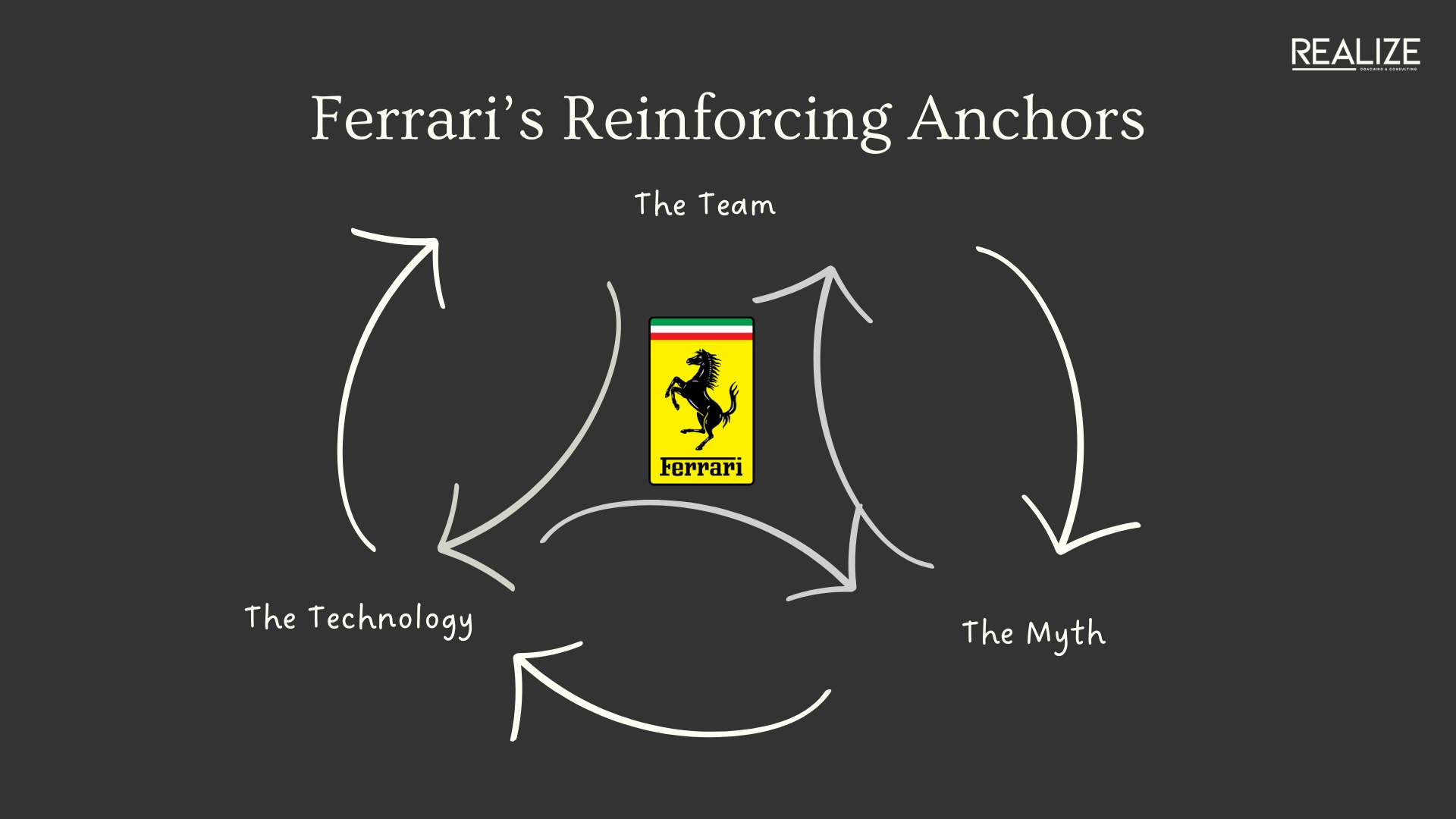

The Intervention: Three Strategic Anchors

When Luca took over, he organized his entire turnaround around three anchors: the team, the technology, and the myth. This is as clean an example of strategic anchors as I have ever seen.

The Team

Luca recruited what is widely considered the greatest Formula 1 team ever assembled: Jean Todt as team principal, Ross Brawn as race engineer, and Michael Schumacher as number-one driver. He understood something profound about racing’s role in the business. As he put it:

“There is not a direct correlation between Ferrari victories on the track and the number of cars that you can sell. But if for many years you do not win, it means that you do not add wood to the fire of the myth. The myth of Ferrari is based on competition. You can win or you can lose, but you cannot only lose.”

The Myth

Luca brought the luxury strategy to Ferrari for the first time. Waitlists, presentation ceremonies, bespoke luggage fitted to each car, geographic segmentation, ruthless scarcity. Most importantly, he cut annual production from 4,500 cars to 2,300 in just two years.

The Technology

Ferrari shifted from being a famously late adopter of new tech to a leading R&D investor in the auto industry. They killed the 348 and replaced it with the 355, an entirely different class of machine. Today Ferrari spends a higher percentage of revenue on R&D than nearly any other car company.

The Flywheel

The genius of these three anchors is how they reinforce each other. Victories on the track add wood to the fire of the myth. The myth justifies extreme pricing and scarcity. Pricing and scarcity fund massive investments in technology. Better technology means the cars actually deliver on the myth’s promise. Cars that deliver create the demand that lets Ferrari stay scarce. Scarcity feeds the myth. And around again.

This is the same shape as the Amazon flywheel and the Disney flywheel I described in the original post. Ferrari is not selling a car. It is operating a self-reinforcing system, where every action the company takes (each new model, each F1 hire, each waitlist decision, each market entry) gets filtered through three questions: does this strengthen the team, advance the technology, or deepen the myth? If not, it does not get prioritized.

The Outputs That Followed

Now we get to the part most people would call the strategy, but which is actually just the scoreboard or operating pulse.

When Luca returned in 1991, Ferrari was worth roughly $192 million. When it IPO’d in 2015, the market cap was $9.8 billion. Today it sits around $55 billion, trading at a P/E multiple on par with Hermès. Gross margins hover around 50%. Profit per car averages over $170,000, meaning Porsche has to sell six cars to match the profit of one average Ferrari. From 2000 to 2004, Schumacher won five straight Drivers’ Championships and Ferrari won five straight Constructors’ Championships.

None of those numbers are the strategy. They are what happens when you get the inputs right.

The Fiat managers before Luca wanted all of those same numbers. They wanted higher revenue, better margins, a more valuable company. What they did not have was a coherent strategy. They had no theory of what Ferrari was committed to being best at, so they defaulted to the most legible levers available (more units, lower costs), and in doing so they nearly destroyed the company. Luca did not chase the outputs. He picked three things to be the best at and let the rest follow.

The Question I Now Ask

When a founder tells me their strategy is to hit a number, I ask the Ferrari question. What are you going to be the best at? What are you committing to that no one else in your category will commit to? What are the three anchors that, taken together, make every other decision in your company coherent and reinforcing?

If you want help articulating the three anchors that should guide your company, book a complimentary session.